A Medicare prospect may love hearing about dental, vision, hearing, over-the-counter benefits, grocery cards, transportation, and gym memberships. But none of those benefits matter much if the client loses access to the doctor they trust most.

That is why smart Medicare agents should consider changing the order of the conversation. Instead of leading with extras, lead with doctors.

Before we compare benefits, let’s make sure we do not accidentally create a doctor problem.

That small shift can change the entire sale. It makes the agent sound less like a salesperson and more like a professional adviser. It also helps prevent the kind of surprise that causes complaints, cancellations, bad reviews, and lost referrals.

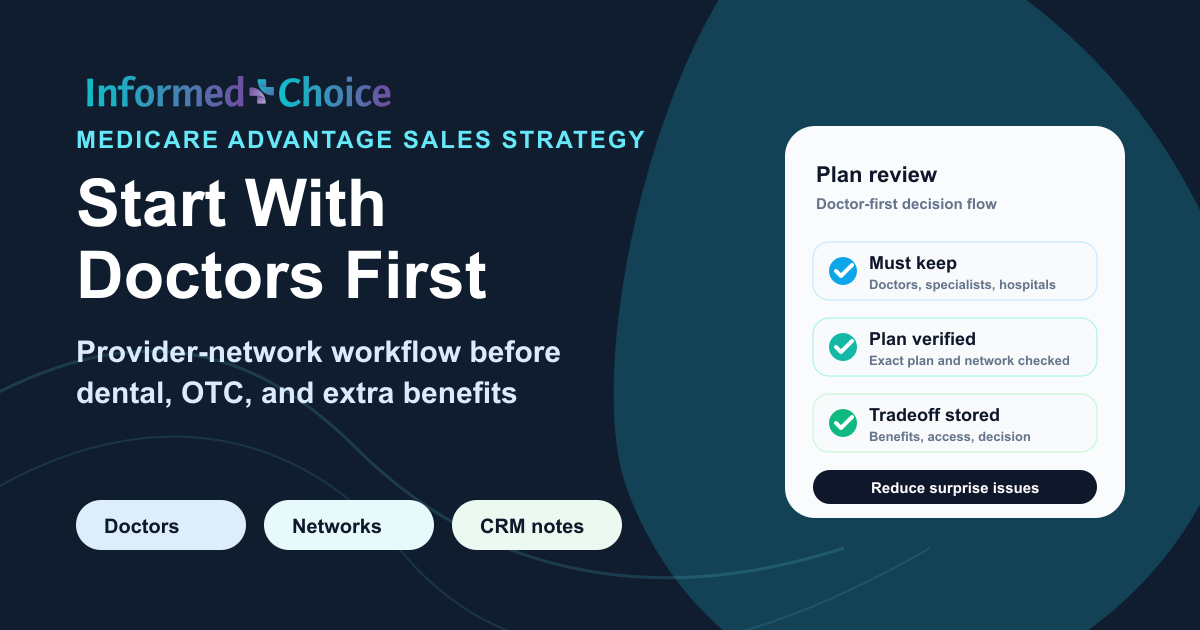

Doctor-first sales workflow

Protect provider access before selling extras

Priority

Ask which doctors, specialists, clinics, or hospitals the client would be upset to lose.

Sort

Separate must-keep providers from nice-to-keep providers before comparing plans.

Verify

Check the exact plan, not just the carrier name, and review facilities, groups, and referrals.

Document

Record the provider checks, tradeoffs, client decision, and follow-up in the CRM.

The Benefit That Gets Attention Is Not Always the Benefit That Protects the Client

Extra benefits are attractive. There is nothing wrong with discussing them. Many clients care deeply about dental coverage, hearing aids, eyeglasses, OTC allowances, and other supplemental benefits. Those benefits can be meaningful, especially for clients on fixed incomes.

But extras are often easy to understand. A client can hear “dental allowance” and immediately picture value. Provider networks are different. Networks are invisible until they become a problem.

The client may not think about whether their cardiologist, oncologist, primary care doctor, orthopedic surgeon, hospital system, or preferred specialist is in network until after enrollment. By then, the agent may be dealing with a very different conversation.

A shiny extra benefit can help close the sale. A missed doctor can destroy the relationship.

The Data Should Get Every Medicare Agent’s Attention

KFF reported that Medicare Advantage enrollees were in plans that included, on average, about 48% of the physicians available to traditional Medicare beneficiaries in the same area in 2022. KFF also found wide county-by-county variation, including large counties where the average share of in-network physicians was much lower.

That does not mean Medicare Advantage is bad. It means Medicare Advantage is local, plan-specific, and network-sensitive. It also means two plans with similar premiums and similar extras may create very different real-world access for the client.

A plan can look good on paper and still be wrong for that person.

- A plan can have attractive extras and still exclude a key provider.

- A plan can have a strong star rating and still have a narrower network than another available plan.

- A plan can fit one neighbor well and still create a problem for the client sitting in front of you.

KFF found that Medicare Advantage star ratings were not correlated with physician network breadth. Star ratings can be useful, but they do not tell the full story for clients who care about access to specific doctors.

The Average Client Is Already Overwhelmed

For 2026, KFF reported that the average Medicare beneficiary had access to 32 Medicare Advantage plans with prescription drug coverage, and 39 Medicare Advantage plans overall for individual enrollment.

That is a lot of options. And when people face too many options, many do not compare carefully at all. KFF reported that nearly 7 in 10 Medicare beneficiaries did not compare their coverage options during a recent open enrollment period. Among Medicare Advantage enrollees, 65% did not compare options.

That is where a good agent earns trust. The agent’s job is not to show every possible plan. The agent’s job is to make the decision clearer. One of the fastest ways to make the decision clearer is to start with the client’s non-negotiables.

The Doctor-First Medicare Conversation

A doctor-first conversation does not ignore premiums, benefits, prescriptions, or plan ratings. It simply puts the client’s health care relationships at the front of the review.

Once the provider list is stable, prescriptions need the same client-specific check. Use the Part D drug-cost review workflow to keep deductible exposure, pharmacy preference, covered drug status, and estimated annual cost from becoming an afterthought.

For Special Needs Plans, confirm eligibility before treating the provider review as a complete recommendation. The D-SNP, C-SNP and I-SNP plan-comparison checklist adds Medicaid alignment, chronic-condition verification, institutional status, facility relationships, and care-management expectations to the doctors-first workflow.

1. Ask the “who can we not lose?” question

Instead of starting with plan features, start with people.

Which doctors, specialists, clinics, or hospitals would you be upset to lose?

That question is better than, “Who are your doctors?” Not every provider has the same emotional or medical importance. A client may have a primary care doctor they like, a cardiologist they need, and a hospital system they strongly prefer. The agent needs to know which relationships are critical and which are flexible.

2. Separate preferred providers from must-keep providers

Create two categories before you start comparing plans.

- Must keep: doctors, specialists, facilities, or clinics the client does not want to lose.

- Nice to keep: providers the client likes but may be willing to change if the overall plan value is better.

This helps the agent avoid overpromising. It also helps the client make a more realistic decision. Sometimes the plan that keeps every provider may not have the lowest premium or richest extras. Sometimes the plan with the best extras may require a provider change. That is not a problem if the client understands the tradeoff before enrolling.

One more boundary matters: a provider-network problem is not automatically an enrollment window. If the client wants to change MA or Part D coverage outside AEP, screen the client’s election-period trigger before moving from plan comparison into an application.

3. Verify the provider carefully

This is where agents can separate themselves from amateurs. Do not rely on vague statements like “they probably take that carrier,” “I think that doctor accepts Medicare Advantage,” or “that medical group usually works with this plan.”

Provider verification should be specific. The agent should verify the exact plan, not just the carrier name. A provider may accept one plan from a carrier but not another plan from the same carrier. A doctor’s office may say, “We take Blue Cross” or “We take UnitedHealthcare,” but that does not always mean they accept the exact Medicare Advantage HMO or PPO being discussed.

Doctor-First Verification Checklist

Use this before presenting extra benefits as the deciding factor.

The Script Agents Should Use

Here is a simple way to explain the issue without scaring the client:

Medicare Advantage plans can offer strong benefits, but the network matters. Before we look at dental, OTC, or extra benefits, I want to make sure the plan does not interfere with the doctors and facilities that matter most to you.

That sounds professional. It also creates a natural reason to slow down the sale. And slowing down the sale can actually increase trust.

What To Say When the Client Only Wants the Extra Benefit

Some clients will still lead with the shiny benefit. They may say, “I just want the plan with the best dental,” “I want the biggest OTC card,” or “My neighbor has a zero-premium plan.”

Do not dismiss that. Acknowledge it, then redirect.

Absolutely, we will compare that. But first I want to make sure the plan does not create a bigger problem. A rich dental benefit is helpful, but not if the plan causes an issue with your doctor, specialist, hospital, or prescriptions.

That is not a hard sell. It is a protective frame. The client hears that the agent is looking out for them.

What To Say When the Client Mentions Star Ratings

Star ratings can be useful, but they are not a substitute for a network check.

That is good information, and we should consider it. But star ratings do not tell us whether your specific doctors are in network. So let’s use the rating as one factor, not the whole decision.

The Three-Part Plan Comparison

After the doctor-first review, agents can simplify the conversation by comparing plans in three categories.

- Option 1: The safest provider-access option. This is the plan that best protects the client’s doctors, specialists, hospital system, or care routine. It may not have the richest extras.

- Option 2: The strongest extra-benefit option. This is the plan with the most attractive supplemental benefits. It may be a good choice if the network, prescriptions, and costs still work.

- Option 3: The balanced option. This may not be the best in every category, but it gives the client a reasonable balance of provider access, prescription coverage, premium, cost-sharing, and extra benefits.

That three-option structure helps the client make a decision without feeling buried under 30-plus plan choices.

The CRM Note Every Agent Should Keep

A doctor-first review also creates better documentation. Agents should consider keeping a simple note in their CRM after each Medicare plan review.

Example CRM Note

- Client priority

- Wants to keep primary care doctor and cardiologist. Dental is important but secondary.

- Providers checked

- Primary care doctor, cardiologist, preferred hospital system.

- Verification source

- Carrier directory and provider office call.

- Plan tradeoff discussed

- Plan A had stronger dental; Plan B better protected current doctors.

- Client decision

- Client selected Plan B after provider-access discussion.

- Follow-up needed

- Confirm ID card received and schedule post-enrollment check-in.

That kind of note is not just a compliance habit. It is a business asset. If the client later forgets why they chose a plan, the agent can remind them of the decision-making process. If there is a dispute, the agent has a clearer record. If the client refers a friend, the agent can repeat a more professional process.

If your agency wants those provider checks, call notes, SOAs, and follow-up records in one agent-controlled place, review how an agent compliance vault can support the record layer around the sales workflow.

Why This Wins More Referrals

Most clients do not refer an agent because the agent gave a generic presentation. They refer an agent because the agent helped them avoid a mistake.

A client may not say, “My agent showed me 23 Medicare Advantage plans.” But they might say, “My agent made sure my cardiologist and hospital were still covered before I switched.”

That is a referral-worthy sentence. The best agents are not just benefit explainers. They are surprise reducers. They help clients avoid the problems the client did not know to ask about.

The Bottom Line

Medicare Advantage sales are not just about showing the richest benefits. They are about helping the client understand tradeoffs.

Dental matters. OTC matters. Premiums matter. Prescription costs matter. Star ratings matter. But for many clients, doctor access matters first.

Before leading with the extra benefit, ask the question that can protect the relationship: Which doctors or hospitals can we not afford to lose?

That one question may separate a transactional agent from a trusted adviser. And in a crowded Medicare market, trusted advisers are the ones clients remember.

This article is for educational purposes only and is not legal advice. Agents should review current CMS guidance, approved scripts, carrier rules, state rules, and agency policies, and consult qualified counsel or compliance professionals for specific requirements.

Get the sale. Keep the client. Keep the proof.

Keep Medicare and ACA records organized in one vault.

Store, retrieve, and export agent-controlled compliance records without scattering files across tools.

Start SOA VaultSources

Frequently Asked Questions

Why should Medicare agents start with doctors instead of dental benefits?

Doctor access is often a client non-negotiable. Dental, OTC, vision, and other extra benefits matter, but a client may regret a plan change if it disrupts their primary care doctor, specialist, clinic, hospital system, or prescriptions.

What should a doctor-first Medicare review include?

A practical review should identify must-keep and nice-to-keep providers, verify the exact plan network, check whether providers accept new patients under that plan, review related facilities and medical groups, and document the tradeoffs discussed with the client.

Do Medicare Advantage star ratings prove a plan has a broad provider network?

No. Star ratings can be useful, but KFF found that Medicare Advantage plan quality star ratings were not correlated with physician network breadth. Agents should treat ratings as one factor, not a substitute for provider verification.

How can agents document a provider-network conversation?

Agents can keep a CRM note that lists the client priority, providers checked, verification source, plan tradeoffs discussed, client decision, and follow-up needed. That record helps explain why the client chose a plan if questions come up later.

Medicare and ACA Compliance Expert

Christian Rodgers is a Medicare and ACA compliance expert with over 30 years in the healthcare industry, having worked for some of the largest health plans in the United States. He has provided Medicare sales training to hundreds of agents in California and Florida.

Connect on LinkedIn