Most health insurance agents are trained to think growth means one thing: more leads. More calls. More appointments. More applications. New business matters, but for many ACA and Medicare agents, the bigger opportunity may be the clients already sitting in the book of business.

Those clients may be confused, auto-renewed, under-reviewed, price-sensitive, or one bad surprise away from leaving. The agent who builds a real renewal system can often outperform the agent who simply spends more money chasing strangers.

That is especially true in the ACA market right now. CMS reported in its January 28, 2026 Marketplace snapshot that about 23.0 million consumers selected 2026 Marketplace coverage. About 19.6 million were returning consumers, compared with about 3.4 million new consumers. That means the 2026 ACA Marketplace was overwhelmingly a returning-customer market, not just a new-enrollment market.

That should change how agents think about growth.

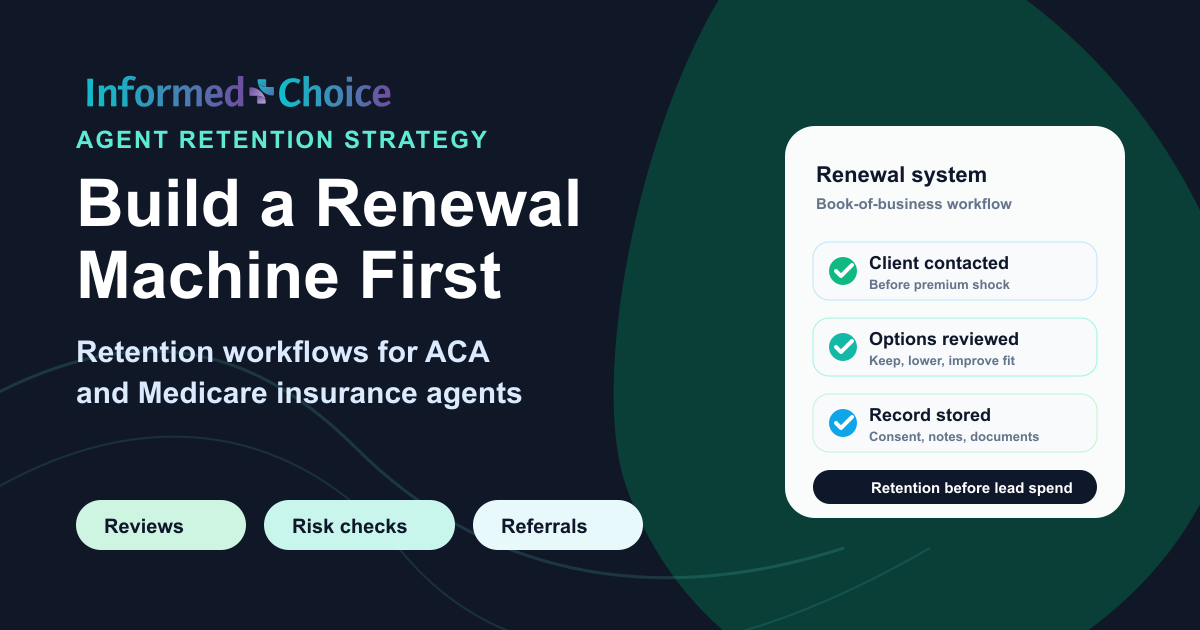

Renewal machine

Turn the book of business into a review system

Segment

Find high-risk clients first: subsidy-sensitive, heavy users, older ACA households, and families.

Contact

Start before frustration: premium, doctors, prescriptions, deductible, and cash-flow risk.

Compare

Show three options: keep current plan, lower premium, or improve fit.

Document

Store notes, consent, application review, plan comparisons, and follow-up records.

Refer

Turn review themes into client education and referral-worthy content.

ACA Is Becoming a Retention Business

For years, many agents treated ACA as a seasonal lead-generation sprint: run ads, buy leads, work Open Enrollment, enroll as many people as possible, and move on.

The data now tell a different story. The Marketplace is mature enough that a huge share of the opportunity is no longer just finding people who have never enrolled before. It is helping existing members make better decisions, avoid bad renewals, understand price changes, and stay properly covered.

That is not just service work. That is revenue protection. It is also trust-building.

A client who hears from you only when it is time to enroll may see you as a transaction. A client who hears from you before a premium shock, network issue, or renewal mistake sees you as an adviser.

The 2026 Premium Shock Made Reviews More Valuable

The expiration of enhanced ACA premium tax credits created a new kind of client conversation. KFF estimated that subsidized Marketplace enrollees who stayed in the same plan could see their premium payments increase by an average of 114% in 2026.

That does not mean every client had the same experience. It does mean agents should expect more confusion, more price sensitivity, and more people asking whether they should switch plans.

The Peterson-KFF Health System Tracker also reported that 70% of respondents said that, if their current premium doubled, they would likely look for a lower-premium Marketplace plan with higher out-of-pocket expenses.

That is the exact moment where a good agent can create value.

Not by saying, “Here is the cheapest plan.” The better conversation is: “Do you want to lower your monthly premium, or would that expose you to more risk when you actually use care?”

The Agent’s Real Job Is to Reduce Bad Surprises

Clients usually do not leave because everything is going well. They leave because something surprises them.

- A higher premium.

- A doctor no longer in network.

- A prescription that moved tiers.

- A deductible they did not understand.

- A plan they were auto-renewed into but never reviewed.

- A bill they thought their insurance would handle.

The agent who prevents surprises becomes hard to replace. That is why every health insurance agent should think of retention as a system, not a task.

A Simple Renewal Machine for ACA Agents

1. Start renewal conversations before clients are frustrated

Do not wait until the client opens a bill and panics. Create a simple renewal calendar. Start with your highest-risk clients first: people with low premiums, subsidy-sensitive households, older ACA clients, families with multiple members on the plan, clients who changed income, and anyone who used care heavily during the year.

Your plan may still be the right fit, but 2026 changed the math for many Marketplace clients. Before you let anything renew, we should check premium, doctors, prescriptions, deductible, and total out-of-pocket exposure.

That message is helpful, not salesy.

2. Stop presenting too many choices

Clients do not need every plan available in the county. They need a clear comparison. One of the easiest ways to improve the review process is to narrow the conversation to three categories.

- Option 1: Keep the current plan. Use this as the baseline. What changes if the client does nothing?

- Option 2: Lower the monthly premium. Show the tradeoff. What deductible, network, prescription, or out-of-pocket exposure changes?

- Option 3: Improve the fit. This may not be the cheapest plan. It may be the plan that better fits doctors, medications, expected usage, or household risk.

That three-option structure makes the conversation easier and helps the client feel guided instead of overwhelmed.

3. Make the review about risk, not just price

Many clients think they are shopping for a premium. They are really choosing where they want to carry risk.

A lower premium can be attractive, especially when budgets are tight. But if the lower-premium plan creates a much higher deductible, weaker prescription coverage, or network problems, the “savings” may not feel like savings later.

A strong agent helps clients compare:

- Monthly premium.

- Deductible.

- Maximum out-of-pocket exposure.

- Doctor access.

- Prescription costs.

- Expected health care usage.

- Household cash-flow risk.

Anyone can quote a premium. Not everyone can explain the tradeoff.

4. Contact auto-renewed clients

Auto-renewal can be convenient, but it can also create false security. A client may assume, “I’m covered, so I’m fine.” Maybe. Maybe not.

CMS explains that returning consumer counts include people who actively selected a plan and people who were automatically re-enrolled. That means many returning clients may not have actively reviewed their options. For agents, that is a major service opportunity.

You may have been renewed automatically, but automatic does not always mean optimal. Let’s make sure your premium, providers, prescriptions, and out-of-pocket exposure still make sense.

5. Turn retention into content

The smartest agents will not only run renewal reviews privately. They will also turn those review themes into public content. That is how retention becomes lead generation.

- Three things to check before letting your ACA plan auto-renew.

- Why the cheapest ACA plan may not be the least expensive plan.

- Premium went up? Here is what to compare before switching.

- Before you change Marketplace plans, check these four things.

- What agents wish every ACA client understood about deductibles.

This type of content attracts better prospects because it demonstrates judgment. It does not scream, “Buy from me.” It says, “I know how to help you avoid mistakes.”

Renewal Review Checklist

Use this as a practical pre-renewal screen before the client lets a plan roll forward.

The Retention Numbers Agents Should Track

Most agents track sales. Fewer agents track retention activity with the same discipline. That is a mistake.

At minimum, agents should track:

- How many renewal clients were contacted.

- How many completed a review.

- How many stayed in their current plan after review.

- How many switched plans after review.

- How many were saved from cancelling.

- How many were referred by existing clients.

- How many complaints or surprise issues came from clients who skipped review.

These numbers show whether the agent has a real book of business or just a list of past transactions.

Why This Also Builds a Better Compliance Culture

This is where practical business advice and compliance finally meet. A strong renewal process naturally encourages better habits: clearer conversations, better documentation, more accurate plan comparisons, provider and prescription checks, and fewer rushed recommendations.

Agents are more likely to listen to compliance advice when they first understand that the same habits also protect their income. Good documentation is not just a regulatory burden. It is also a business asset.

A clear review process protects the client, protects the agent, and improves the quality of the recommendation. If you need a place to keep ACA consent, eligibility application review notes, and related Marketplace files together, review how the ACA Compliance Vault supports agent-controlled recordkeeping.

The Bottom Line

The agents who win the next phase of the health insurance market will not simply be the agents who buy the most leads. They will be the agents who build the most trust.

That trust is built through review systems, not random check-ins. It is built by reducing surprises. It is built by explaining tradeoffs clearly. It is built by helping clients make decisions before they are frustrated.

New leads matter. But your existing book may be the most underused growth engine in your business.

Before you spend more money chasing the next lead, ask a harder question: Do I have a renewal machine, or do I just have a list of people I enrolled last year?

This article is for educational purposes only and is not legal advice. Agents should review current CMS guidance, carrier rules, state rules, and agency policies, and consult qualified counsel or compliance professionals for specific requirements.

Keep Medicare and ACA records organized in one vault.

Store, retrieve, and export agent-controlled compliance records without scattering files across tools.

Start SOA VaultSources

Frequently Asked Questions

Why should insurance agents focus on renewals before buying more leads?

Renewals protect the book of business agents have already built. A structured review process can reduce surprise cancellations, create better client conversations, and turn existing clients into referral sources before the agent spends more on cold acquisition.

What should an ACA renewal review include?

A practical ACA renewal review should compare the current plan, a lower-premium alternative, and a better-fit option across premium, deductible, maximum out-of-pocket exposure, provider access, prescription costs, expected usage, and household cash-flow risk.

Should agents contact auto-renewed ACA clients?

Yes. Auto-renewal can keep a client covered, but it does not mean the plan is still optimal. Agents should contact auto-renewed clients to review premiums, providers, prescriptions, deductibles, and out-of-pocket exposure before problems appear.

How does retention content help generate new leads?

Content about renewal mistakes, premium changes, deductibles, provider checks, and auto-renewal shows prospects that the agent understands real client risk. That can attract better prospects because it demonstrates judgment instead of only asking for a sale.

Medicare Compliance Expert

Christian Rodgers is a Medicare compliance expert with over 30 years in the healthcare industry, having worked for some of the largest health plans in the United States. He has provided Medicare sales training to hundreds of agents in California and Florida.

Connect on LinkedIn